India’s Green Molecules Moment: ACME’s New Deals Show the Market Is Finally Moving from Announcements to Offtake

Tokyo has moved from ambition to allocation. For project developers and oil & gas, the way Japan structured its first hydrogen awards matters more than any headline target. When Japan published the world's first national hydrogen strategy in 2017, the insight was never really about technology. It was about sequencing. Most governments waited for clean molecules to become cheap and then hoped demand would appear. Japan, a resource-constrained importer with no illusions about producing its own way to energy security, did the opposite. It set out to manufacture demand — and to make that demand bankable enough that someone else would build the supply. For years that looked like patient theory. In late 2025 it became spending. What Japan actually built The framework is the Hydrogen Society Promotion Act, passed in May 2024 and in force from October 2024. It does two things that should be familiar to anyone who has financed infrastructure. First, a Contract for Difference (CfD) , administered by JOGMEC, that pays the gap between the cost of low-carbon hydrogen and its derivatives and the price of the conventional fuels they displace. The government has earmarked roughly ¥3 trillion — about US$19bn — with support running for terms of up to 15 years. This is the same instrument that de-risked offshore wind in the UK, repurposed for molecules: a long-dated, predictable revenue floor that lets a developer underwrite capital against something other than a volatile spot price. Second, a hub support scheme that co-funds the shared receiving terminals, storage and pipelines that no single offtaker will build alone — backed by the long-standing financing muscle of JOGMEC, JBIC and NEXI. Around these sit the targets: roughly 3 million tonnes of hydrogen (including ammonia) by 2030, 12 million tonnes by 2040, and 20 million by 2050, with CIF cost targets stepping down to around 20 yen/Nm³ by mid-century. Crucially, Japan defines eligibility by carbon intensity, not colour — a clean-hydrogen threshold around 3.4 kg CO₂/kg H₂ (well-to-gate) and a low-carbon ammonia threshold near 0.84 kg CO₂/kg NH₃ (gate-to-gate). Any molecule that clears the bar competes. That last design choice is the one developers keep underweighting. It is the difference between a market that buys virtue and a market that buys delivery. The first cheques, and what they signal After a slow start, the first awards landed in 2025: two small domestic projects in September, and then the one that mattered — the first international award in October, to JERA and Mitsui for blue ammonia from the Blue Point project in Louisiana, developed with CF Industries. JERA takes 0.5 Mtpa from early 2030, largely for co-firing at its Hekinan coal plant; Mitsui takes 0.28 Mtpa from 2031 for Hokkaido Electric, with volumes also going to cement and chemicals. Together that is around 772,000 tonnes of ammonia a year — roughly 120,000 tonnes of hydrogen equivalent — locked under 15-year CfDs. Wood Mackenzie estimates the two deals absorb about US$6.8bn, leaving roughly two-thirds of the pool unallocated, and called the round "a breakthrough, not a conclusion." Energy Intelligence reports the Middle East and India are already on Tokyo's radar for what comes next. For developers and oil & gas, three signals are doing the real work here. One: blue beat green . The flagship overseas molecule is blue ammonia, chosen on cost, scale and the certainty of an existing US gas-and-CCS value chain. Green developers are not competing against other green developers for these tonnes. They are competing against blue, on a blended test of carbon intensity, price and deliverability. Anyone marketing on colour rather than on a number and a delivery date is reading the wrong rulebook. Two: the anchor end-use is contested. Japan's near-term demand leans heavily on ammonia co-firing in thermal power — the most criticised application in the sector. BloombergNEF has long argued that retrofitting coal to co-fire ammonia lands above US$136/MWh at a 50% blend by 2030, dearer than renewables paired with storage, with nitrous-oxide risks attached. TransitionZero finds that a 20% co-firing plant can emit more than unabated gas across parts of Asia. A December 2025 Kiko Network analysis put the lifecycle CO₂ reduction at a 20% blend at only about 12%. The counter-case is genuine — co-firing uses existing assets, creates bulk demand quickly, and can pull a supply chain into existence faster than a purist pathway would — but developers should treat power-sector co-firing as a demand signal with a visible expiry risk, and prize offtake into fertiliser, chemicals, steel, shipping and refining, where the molecule is harder to substitute. Three: the subsidy accrues to the importer. The price-gap support is claimed on the Japanese side of the customs border. A foreign producer rarely captures it directly; value flows through the offtaker or the importing entity. That makes contract architecture — who holds the CfD, how the gap is shared, how indexation and FX are handled — as decisive as the levelised cost of the plant itself. Why oil & gas should recognise this playbook None of this should feel foreign to the hydrocarbon industry. A long-dated price-gap contract is a tolling-style revenue floor. The Blue Point structure — a producer plus equity-holding offtakers plus a sovereign-backed subsidy — is the integrated gas-to-LNG model rebuilt for molecules: take equity in production, lock the offtake, and let a creditworthy demand centre underwrite the chain. Trading houses are doing what trading houses do, intermediating volume and risk. For oil & gas balance sheets that already know how to finance multi-decade offtake against a sovereign demand signal, Japan has effectively published the term sheet. The newer skill is carbon-intensity accounting and certification, which now sit inside the bankability test rather than beside it. The India lens For India this is opportunity and warning in one document. India's green ammonia, proven through competitive SECI auctions and offtakes such as AM Green–Uniper, is among the lowest-cost in the world. India's new MNRE green ammonia standard of 0.38 kg CO₂e/kg NH₃ — though measured over a different system boundary than Japan's gate-to-gate figure — is strict enough that genuinely green Indian product should clear most international buyers' thresholds comfortably. The mechanisms to monetise the carbon story exist too, including Japan's Joint Crediting Mechanism for Article 6 credits. The warning is in the first picks: they went to blue, and to the United States. Cost-competitiveness is the entry ticket, not the win. Converting India's advantage into Japanese tonnes will demand bankable, long-dated, RFNBO-grade certified offtake contracts, structured so that Indian suppliers capture value on the right side of an importer-side subsidy — and it will demand moving before the unallocated two-thirds of the pool is spent. The real lesson The draft thesis is correct: hydrogen transitions will be shaped as much by market design and policy certainty as by technological innovation. Japan has now proved it with money. But the sharper, more useful version for anyone building or financing a project is this: whoever designs the market writes the rules of competition. Japan's rules reward carbon intensity within a threshold, cost, certification and delivery — not ambition, and not colour. Technology may enable the hydrogen transition. Market architecture will decide who scales within it — and, increasingly, who gets paid. Sources informing this piece include METI/JOGMEC and the Hydrogen Society Promotion Act framework; Wood Mackenzie, BloombergNEF, TransitionZero, Kiko Network, Energy Intelligence and S&P Global commentary; and India's MNRE Green Ammonia Standard (Feb 2026). Figures are as reported at the time of writing and should be re-verified before publication.

The IMO’s Marine Environment Protection Committee is meeting in London for its 84th session from 27 April to 1 May 2026. The final IMO press release and plenary confirmation are still awaited at the time of writing. This note is therefore based on working group documents available from within the session, particularly MEPC 84/WP.5, WP.6, WP.7 and WP.8, dated 27–30 April 2026. IMO’s official preview confirms that MEPC 84 is considering key implementation work on greenhouse gas reduction, marine fuel lifecycle guidelines, biofuels, and the proposed North-East Atlantic Emission Control Area. For India, the message is clear: the regulatory case for green hydrogen-derived marine fuels is becoming stronger. Even while the IMO Net-Zero Framework remains politically contested, the direction of travel is unmistakable. Shipowners serving India–Europe routes will face a growing stack of compliance obligations under EU ETS, FuelEU Maritime, tighter IMO fuel certification rules, and potentially a new North-East Atlantic Emission Control Area.

The Indian developer quietly building one of the most advanced green ammonia portfolios The global hydrogen economy is still in its formative stage. Across the world, hundreds of projects have been announced, but only a handful are moving steadily toward construction, contracting and eventual operation. Among those developers pushing ahead is ACME Group - a GH2 India Anchor Member - that has assembled what is now widely seen as one of the most advanced portfolios of green hydrogen and green ammonia projects globally. With projects spanning India and the Middle East, ACME represents a generation of developers that began preparing for the hydrogen economy well before it became central to government policy or global climate strategies. Today, as hydrogen markets begin shifting from ambition to execution, that early conviction is beginning to show results. Duqm, Oman One of the world’s first commercial green ammonia export projects ACME’s most prominent development is its Green Hydrogen and Green Ammonia facility in Duqm, Oman, one of the most advanced hydrogen export projects currently under development. The first phase of the project will supply 100,000 tonnes of green ammonia annually to Norwegian fertiliser company Yara under a long-term offtake agreement. The first deliveries are expected in Q1 2027, which would position ACME to become the first Indian company to export green ammonia to Europe at commercial scale. The Duqm project sits within Oman’s rapidly developing hydrogen ecosystem. The country has emerged as a strategic location for large-scale hydrogen production, benefiting from abundant solar and wind resources, deep-water port infrastructure and proximity to global shipping routes. For ACME, Duqm represents more than a single project. It forms part of a broader vision of future clean energy trade corridors, where renewable-rich regions supply hydrogen derivatives such as ammonia to industrial demand centres across Europe and Asia. As global demand grows for low-carbon fuels in sectors such as fertilisers, shipping and heavy industry, these trade corridors are expected to become a defining feature of the hydrogen economy.

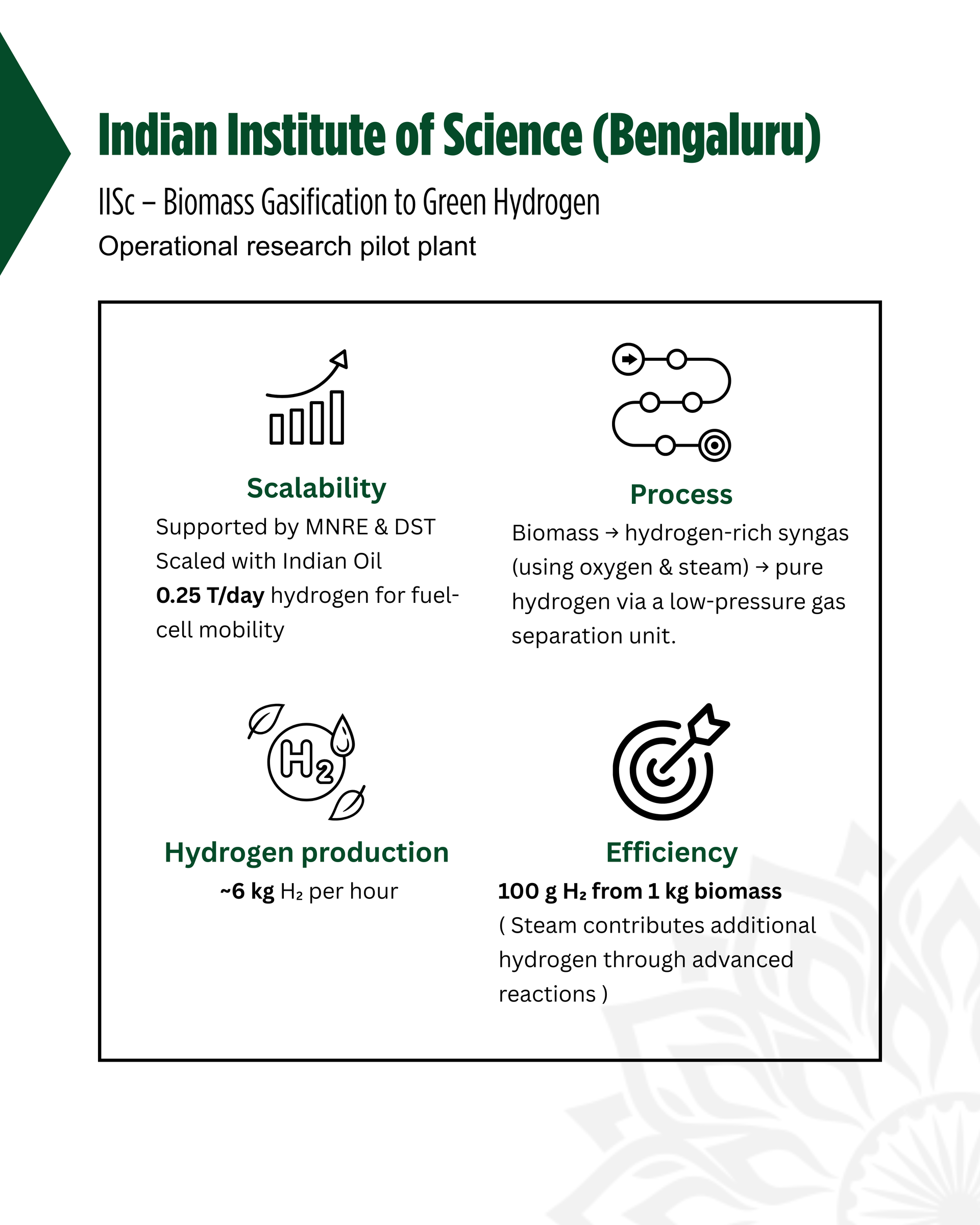

Turning Residues into Fuel: Why Biomass Matters to India’s Hydrogen Pathway India’s hydrogen transition cannot rest on electrolysis alone. While renewable-powered electrolysis remains central to long-term decarbonisation, it is capital-intensive, grid-dependent, and constrained by freshwater availability. A parallel pathway is therefore emerging, one that is indigenous, decentralised, and rooted in India’s agrarian economy: biomass-to-hydrogen. India generates hundreds of millions of tonnes of agricultural and organic residues annually by paddy straw, bagasse, crop stubble, forestry waste, and municipal biogenic waste. A significant share of this is either burned or left to decay, contributing to air pollution, methane emissions, and local environmental degradation. Converting these residues into hydrogen addresses two systemic challenges at once: waste management and clean fuel production. Unlike water electrolysis, biomass-based hydrogen does not primarily depend on electricity. Instead, it leverages thermochemical and biological conversion routes, gasification, dark fermentation, and novel digestion processes to extract hydrogen from carbon-rich waste streams. While these technologies are at earlier Technology Readiness Levels (TRLs) than electrolysers and often less energy-efficient on a pure output basis, they deliver something electrolysis cannot: pollution abatement at source and rural value creation. This makes biomass-to-hydrogen not just a technological choice, but a strategic industrial and environmental intervention. What the Early Pilots Are Demonstrating A small but significant set of pilots is testing different technological pathways and business models. Together, they illustrate the diversity and complexity of India’s biomass opportunity.

Building an India–Europe Green Hydrogen Corridor AM Green, an anchor member of GH2 India, has signed a long-term offtake agreement with Germany-based energy company Uniper for the supply of up to 500,000 tonnes per annum of renewable ammonia from India. Among the largest green ammonia offtake arrangements announced to date, the agreement marks a significant step in positioning India as a reliable global supplier of green hydrogen derivatives. The partnership strengthens the emergence of an India–Europe green hydrogen corridor, with renewable ammonia expected to play a critical role in decarbonising hard-to-abate sectors such as power generation, chemicals, and heavy industry. First deliveries under the agreement are expected to commence around 2028, subject to project development and commissioning timelines.

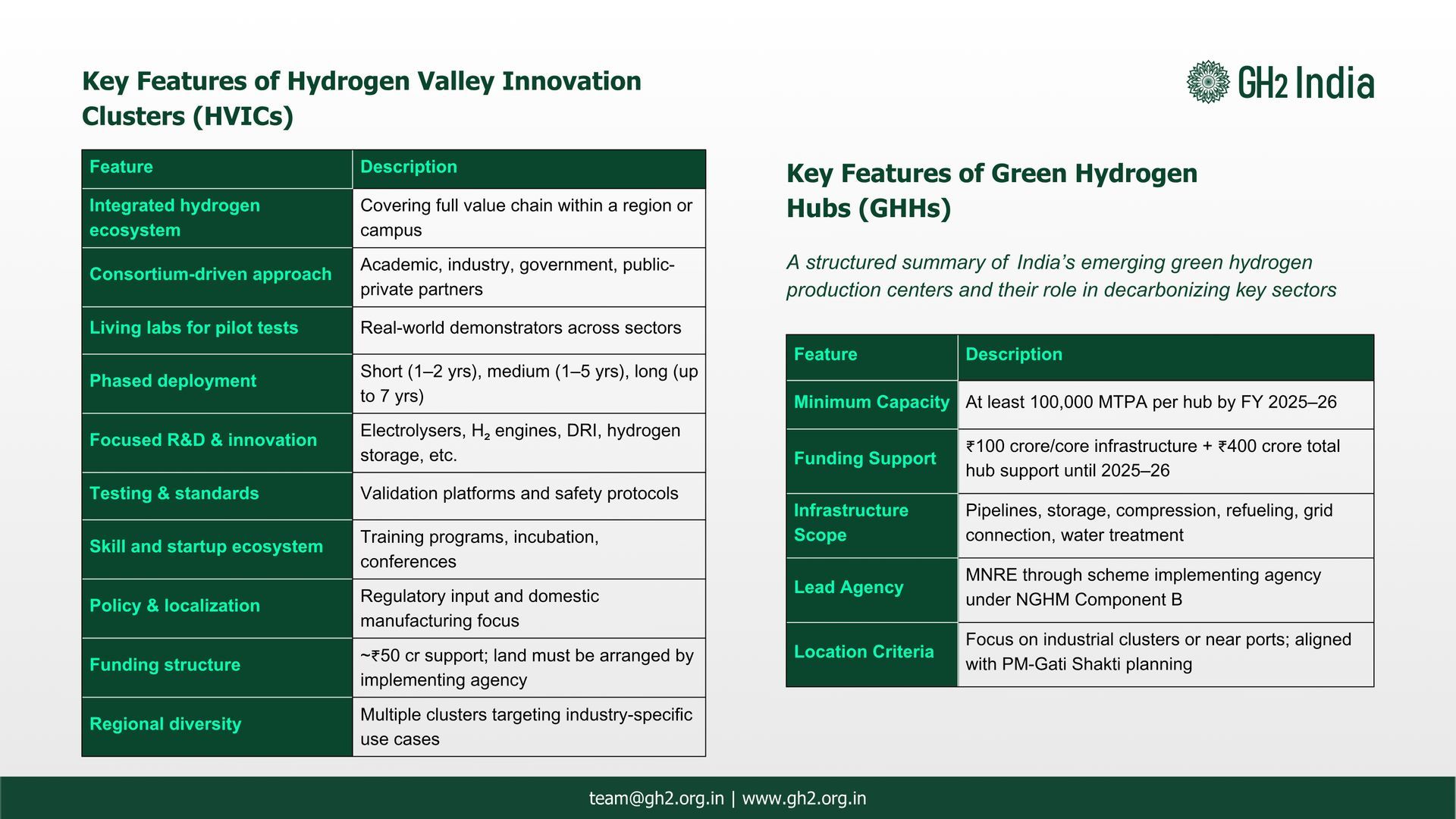

The Ministry of New and Renewable Energy (Hydrogen Division) (MNRE) last month released a set of guidelines on setting up Green Hydrogen Hubs (GHH) and Hydrogen Valley Innovation Centres (HVIC) across the country, pursuant to the goals enlisted in the National Green Hydrogen Mission to boost business innovation around the green hydrogen The Guidelines lay down a detailed roadmap for the development of the GHHs and the HVICs including objectives, implementation methodologies and authorities as well as expenditure schemes. The Guidelines envision HVICs as ‘test beds’ or ‘living labs’ for facilitating innovations in green hydrogen across diverse fields, facilitating experiential learning and deriving insights from existing hydrogen pilot projects. They will also foreground business models, map out techno-economic viability of hydrogen projects and foster strategic partnerships between hydrogen producers and off-takers. Based on the outcome of the HVIC, regulatory framework and policies shall be framed subsequently to further accelerate the development of hydrogen-based projects and realise the goals under the NGHM. HVICs have also been tasked with developing the capacity to localise and integrate the entire green hydrogen value chain, generate demand, and secure uptake for end-use of the hydrogen applications. HVICs must also arrange for the acquisition of land for the project. The funds endowed for this will not cover land acquisition and setting up costs. The guidelines further contemplate hydrogen hubs as an ecosystem of hydrogen producers, end-users, and adequate supporting infrastructure including storage, transportation, and processing facilities based around a particular geographical region. They may be located either close to ports or inland. Areas with clusters of refineries, fertilisers and other end-use industries also have been identified as preferred locations for hydrogen hubs. The guidelines have set a target production capacity of 100000 Metric Tonnes Per Annum of green hydrogen per hub. All key resources of the hydrogen hubs, including infrastructure and project development, will be mapped under the PM Gati Shakti portal. MNRE has further outlined the details of the implementation of these guidelines in its Annexure. The authority to oversee the implementation of the HVIC will be a Scheme Implementing Agency (SIA) of the Department of Science and Technology while a SIA nominated by MNRE will be responsible for the execution of the GHH. While the guidelines provide an impetus for innovation driven developments in India’s green hydrogen economy, a few causes of uncertainty have also arisen in the recent past. The Solar Energy Corporation’s (SECI) announced the cancellation of the tender for setting up green hydrogen hubs on July 4, 2025, and stated that all the tender management fees or document fees submitted thus far will be refunded. Bidders have been advised to email the concerned persons at SECI with the required documents seeking the refund before July 20, 2025. While no official reason has been released by the government on this matter yet, this has raised questions about the future trajectory of India’s green hydrogen goals as we draw near 2030.

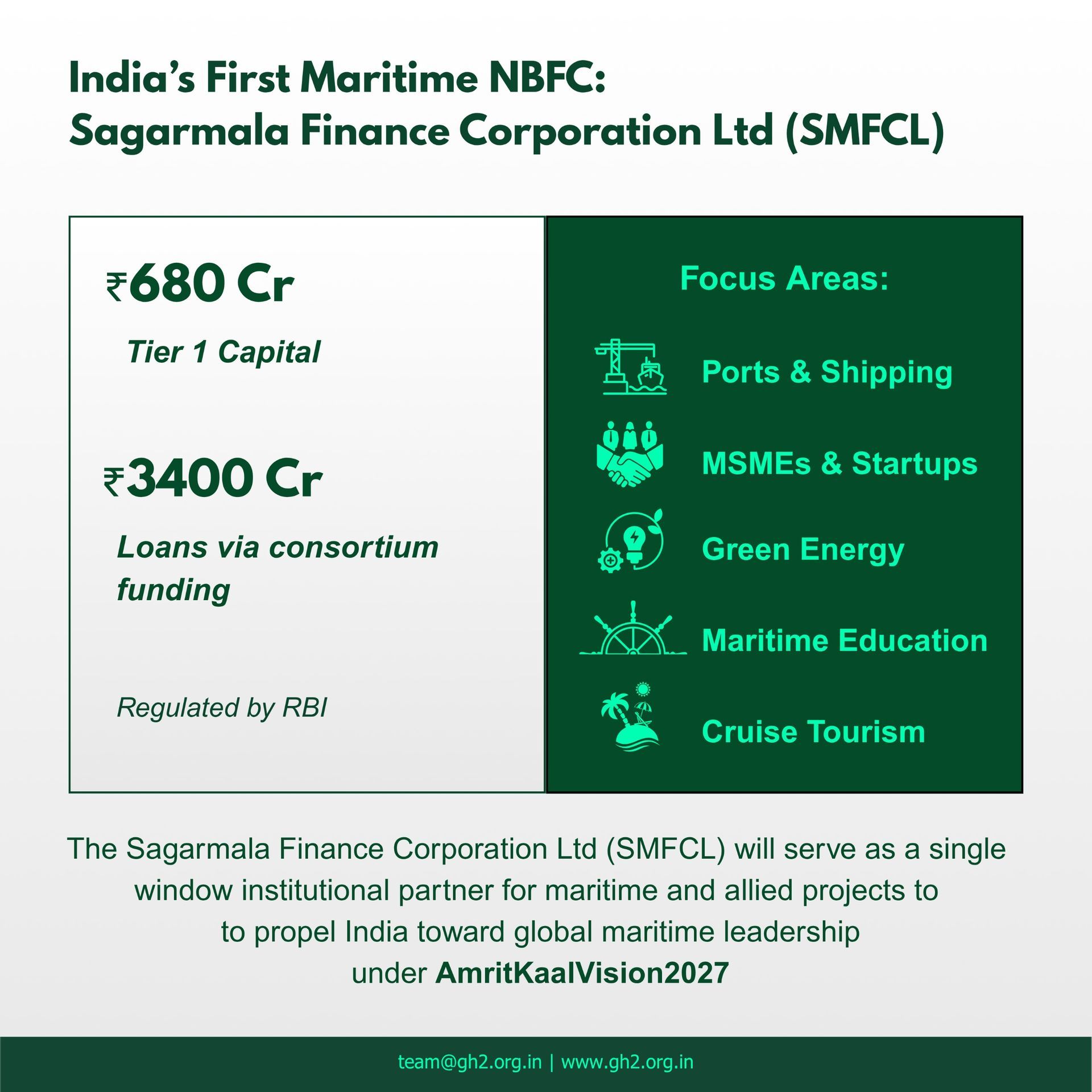

Last week the Hon’ble Union Minister of Ports, Shipping and Waterways, Shri Sarbananda Sonowal unveiled the Sagarmala Finance Corporation Limited (SMFCL), the first of its kind Non-Banking Financial Company (NBFC) exclusively for the maritime sector. In its previous avatar as the Sagarmala Development Company Limited, SMFCL was the key implementing entity for the Sagarmala Programme, encompassing project development and formulation to fund raising and Coastal Economic Zones master plan, among others. This remodelling comes as a response to the long-standing demand of the maritime industry for a sector specific financing institution and is in alignment with India’s goal to emerge as a global maritime leader under the Amrit Kaal Vision 2027. On account of the maritime industry being a capital-intensive sector which is slow to yield returns with regulatory strictures, investment prospects are often limited. This risky and yet niche sector struggled to procure private lending from banks and private investors and thus the need for a unified financial institution dedicated just to the marine industry was reinforced. On June 19, 2025 SMFCL was formally registered as an NFBC with the Reserve Bank of India (RBI) and is categorised as a Mini Ratna, Category I, Central Public Sector Enterprise. With the Tier 1 capital estimated at Rs 680 crore, SMFCL has the capacity to offer bigger loans with consortium partners, valuing up to Rs 3400 crores. With the objective of bridging the financial gaps in the maritime industry, SFMCL will provide financial support towards empowering ports, MSMEs, startups, and maritime educational institutions. As a dedicated financing body, SFMCL is poised to usher in significant transformation in the maritime sector and accelerate industry wide growth, sustainability and innovation. It will also extend to strategic sectors like shipbuilding, renewable energy, cruise tourism, and maritime education. Overall, by enabling access to a focused financial opportunity, SFMCL will leverage efficiencies and inclusive development in the maritime sector, thus propelling India towards global maritime leadership. Built akin to other successful development financial institutions in India like the Indian Railway Finance Corporation for the railways, SMFCL comes with an expanded funding horizon and several other essential services. These include blended finance instruments like equity, subordinated debts, debts etc. It will also support Private Public Partnerships (PPPs) in financing logistics corridor, coastal infrastructure among others. SMFCL’s founding is a critical step towards steering India’s maritime sector at par with the global standards. The European Commission launched the Ship Financing Portal in July 2024, serving as a centralized repository of financing products for the EU-based maritime sector. This is complemented by European Investment Bank’s (EIB) co-financing maritime sector project. Similarly, in Japan, the SMBC Group operates a global maritime finance division, leveraging its strong balance sheet and institutional dedication to the shipping industry to provide long-term support. SMFCL is not only likely to help the maritime industry overcome the financial bottlenecks but also will greatly boost the green transition in the maritime industry, as envisioned in India ’Gateway to Green roadmap. Streamlined funding will help amplify green hydrogen capacity at ports and bunkering stations, and enable shore power infrastructure, etc. This brings in the much-needed transformation to the erstwhile fragmented investment space for the maritime industry and enables SMFCL to cater to the unique capital requirements of the maritime and shipping sector.

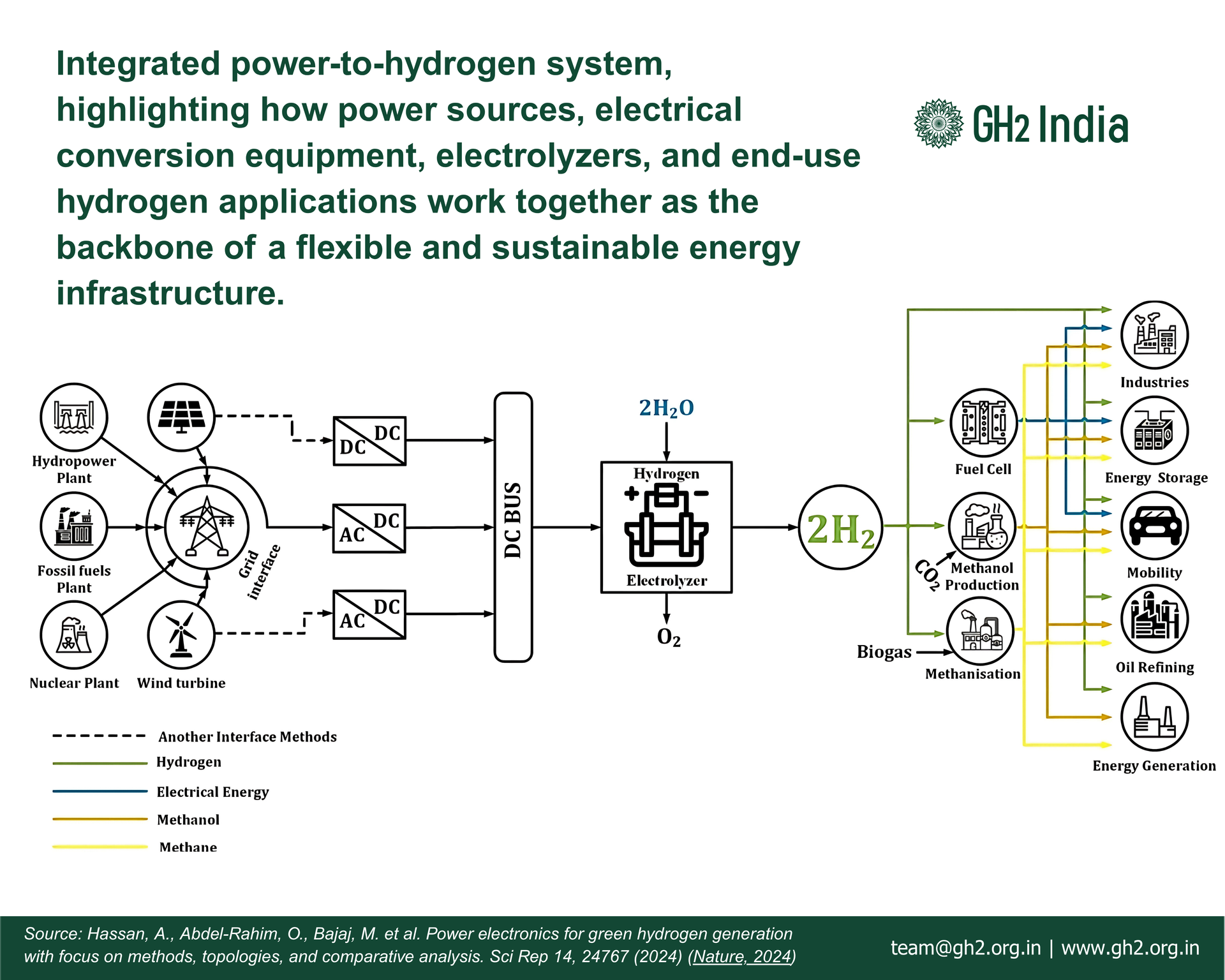

India has committed to producing 5 million tonnes of green hydrogen per year by 2030, supported by approximately 125 GW of new renewable generation capacity (CEEW, 2024). Yet behind this high-profile ambition lies a less discussed but arguably more decisive factor: the vast electrical infrastructure required to turn fluctuating renewable electricity into the stable, precisely controlled DC power that electrolyzers need. This is the real machinery that converts photons and winds into hydrogen molecules, and it is expensive, complex, and often invisible in public debates (Iris CNR, 2024). Today, India’s green hydrogen costs hover between ₹397–₹560 per kilogram ($4.6–$6.7/kg) , which is two to three times the cost of grey hydrogen produced from natural gas. Nearly 95% of this cost is tied to capital investment and financing , and within that, 30–50% comes from electrical systems alone. For a single 100 MW PEM electrolyzer project , that means ₹1,000–1,200 crore ($120–145 million) just in transformers, rectifiers, converters, switchgear, sensors, and control systems (CEEW, 2024). In other words, the electrons are not only expensive because renewable power isn’t free, but they are also expensive because they must be processed, stabilized, and delivered with extraordinary precision. Hydrogen electrolysis is an energy-intensive process, requiring 50–55 kWh/kg H₂ including losses (Iris CNR, 2024). Of this, power conversion losses typically account for 1–2 kWh/kg, equivalent to 2–4% of total energy input. Technical benchmarks help illustrate what’s at stake: Thyristor-based SCR rectifiers achieve >98.5–99% efficiency at full load but suffer poor power factor (<0.7) and up to 30% total harmonic distortion (THD) if not mitigated with filters. Active front-end IGBT converters deliver 96–97% efficiency but maintain near-unity power factor and <5% THD (ResearchGate, 2024). A 100 MW electrolyzer operating 7,000 hours/year will consume 700 GWh/year of AC input. If conversion losses are reduced from 4% to 2%, the plant saves 14 GWh/year, translating to ₹70–85 crore/year at industrial tariff rates (~₹5–6/unit). Ripple reduction is equally critical: PEM stacks degrade faster under >5% DC ripple. High-frequency interleaved DC-DC converters can cut ripple below 1%, extending stack life from ~60,000 to ~80,000 hours (Iris CNR, 2024).

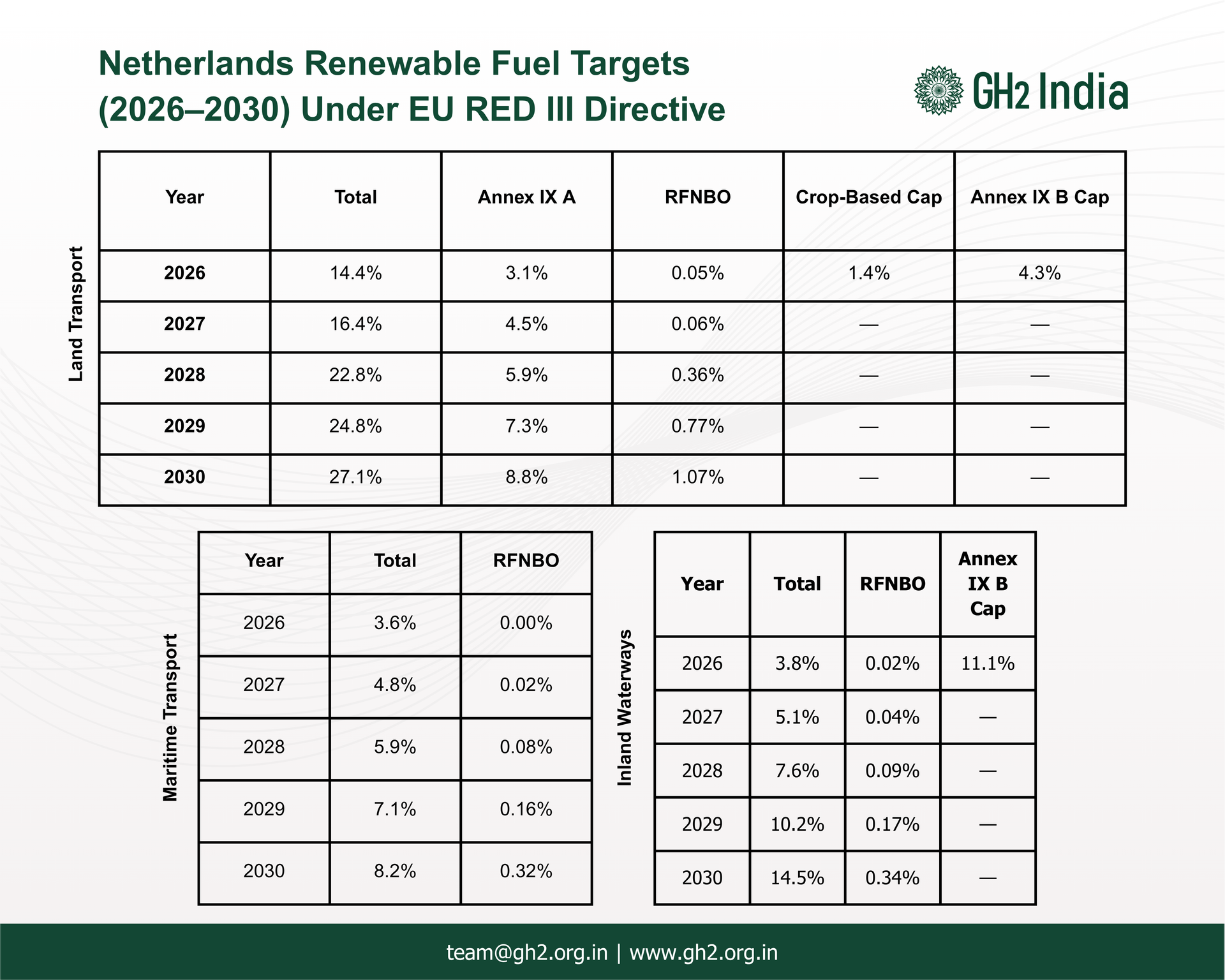

On 24 June 2025, the Dutch Ministry for Infrastructure and Water Management released the draft “Implementation of RED III” regulation to transpose the EU’s Renewable Energy Directive III. This draft outlines obligations for renewable energy uptake in the transport sectors, land, inland shipping, and maritime, while notably excluding aviation. This is aimed at eschewing instances of double counting of renewable energy contributions from raw materials enlisted under Annex IX of RED II. It follows an EU Commission request to comply by 25 May 2025 on setting designated acceleration zones and further aligning with EU timelines (implementation beginning in 2026) The proposal mandates a phased increase in the share of renewable energy in transport fuels, from 14.4% in 2026 to 27.1% by 2030, using a GHG-based accounting system referred to as Energy Reduction Units. Obligated suppliers, with overall consumption more than 500,000/year, will be required to surrender EREs annually. While EREs from the land transport sector can be used to meet shipping obligations, the reverse will not be permitted. The draft sets a cap on crop-based biofuels at 1.2% of total energy for the land sector, consistent through 2030. For biofuels based on Annexe IX Part B feedstocks such as used cooking oil and animal fats, the land sector is capped at 4.29%, inland shipping at 11.07%, and the maritime sector is excluded altogether. The Dutch government has also opted to decouple the EU-wide 5.5% advanced biofuels and 1% RFNBO sub-targets, allowing them to be met separately. Renewable hydrogen used in refineries will count towards a separate RAREs (Refinery Assigned Reduction Effort) obligation, offering another pathway for compliance. A hydrogen “correction factor”, which would reduce the creditable value of hydrogen as a fuel, will not be applied in the near term, and may only be introduced after 2030, reflecting the government’s commitment to support the direct use of hydrogen. To maintain fuel quality standards, the Netherlands will retain its current B7 biodiesel blend limit, despite EU provisions allowing up to B10, citing concerns about compatibility with older diesel vehicles. The existing Dutch renewable fuel credit system, known as HBEs, will be converted into EREs effective from 1 April 2026. Credit banking will be allowed, with a limit of 10% for obligated parties and 4% for registered entities. The phased renewable energy targets and crediting mechanisms provide regulatory clarity for investors and market participants. For India, the clear caps on conventional feedstocks, combined with rising RFNBO and advanced biofuel targets, signal a growing demand for renewable hydrogen and synthetic fuels within the EU. This may make it exigent to re-adjust our focus from the existing cooking oil and animal fat markets towards investments in advanced biofuels. The delay in applying a correction factor for hydrogen further strengthens the case for direct hydrogen use, particularly in refining applications. These provisions align well with India’s strengths in low-cost renewable hydrogen production and create a scope for technology transfer, supply partnerships, and strategic advisory roles targeting Europe’s evolving clean fuels market. This draft regulation provides clarity on the Netherlands’ implementation approach and introduces a structured compliance mechanism that emphasizes the role of advanced biofuels and renewable hydrogen in transport decarbonization. For emerging producers and exporters of renewable hydrogen and e-fuels, including Indian developers, this framework offers regulatory signals worth monitoring closely.